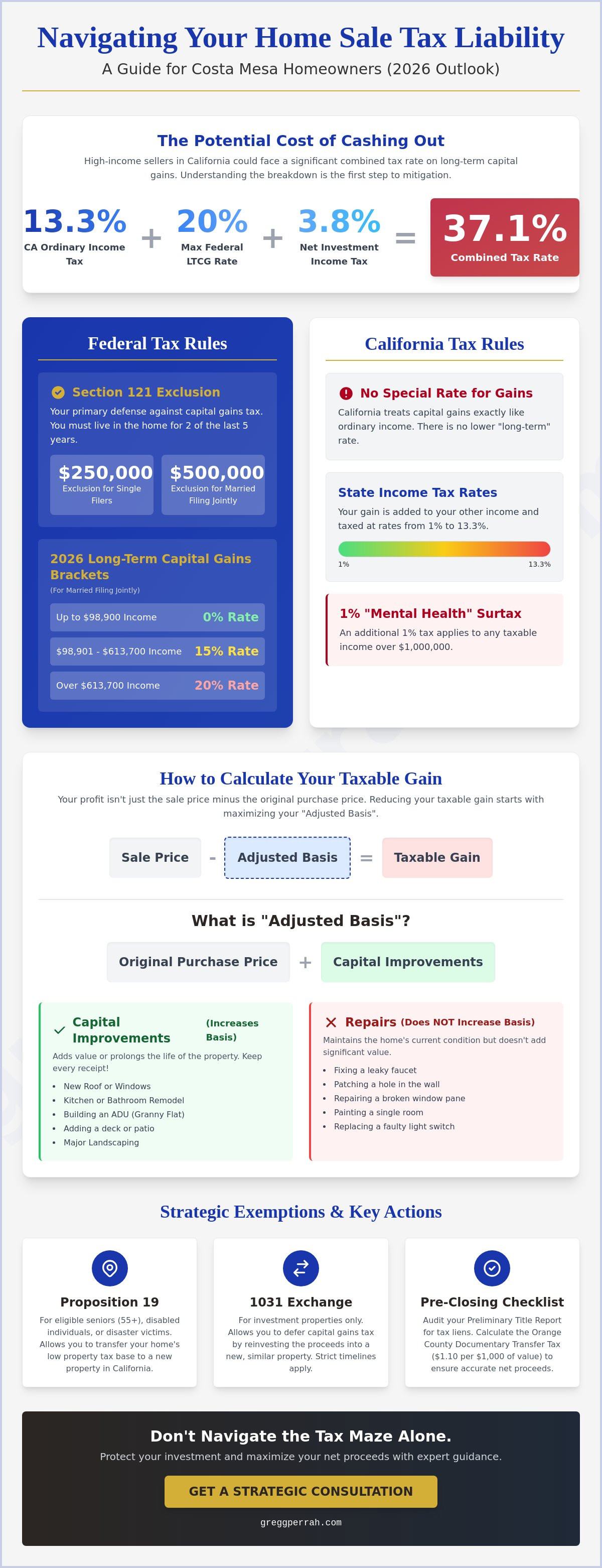

Did you know that a high-income seller in California could face a combined tax hit of 37.1% on their long-term capital gains in 2026? It's a staggering figure that catches many homeowners off guard at the closing table. You've spent years building equity in your property, and the fear of a massive, unexpected tax bill is completely valid. California's tax system is notoriously complex because it treats all capital gains as ordinary income, regardless of how long you've owned the asset.

Understanding the specific tax implications of selling a home in Costa Mesa is the only way to ensure you don't hand over more than your fair share to the IRS or the Franchise Tax Board. I'm here to provide the seasoned authority and expert guidance you need to protect your investment and maximize your net proceeds. This article gives you a clear roadmap to estimate your potential liability while revealing legal strategies to defer or exclude gains entirely. We'll break down the 2026 federal exclusion limits, explain how Proposition 19 affects your property tax base, and explore how a 1031 exchange can keep your wealth growing.

Key Takeaways

- Master the federal Section 121 exclusion and California’s specific income tax rates to accurately forecast the tax implications of selling a home in Costa Mesa.

- Track every capital improvement receipt to boost your adjusted basis and legally minimize the profit subject to federal and state taxation.

- Calculate the Orange County Documentary Transfer Tax early to ensure your net proceeds estimate remains accurate through the final settlement.

- Seize the benefits of Proposition 19 or 1031 exchange strategies to protect your home equity and maintain your lifestyle during a transition.

- Audit your Preliminary Title Report for potential tax liens to ensure a seamless, high-speed closing in today’s competitive market.

The Foundation: Federal and California Capital Gains Rules in 2026

What is the real cost of your exit? When you sell your Costa Mesa home, the difference between your sales price and your "basis" is your capital gain. The government views this profit as taxable income. Protect your equity by mastering the Federal Capital Gains Rules. For 2026, your primary defense against a massive bill is the Section 121 exclusion. This is the most powerful tool in your financial arsenal.

Are you filing single or married? Single filers can exclude up to $250,000 of gain. Married couples filing jointly can exclude $500,000. This isn't just a guideline; it's a massive financial shield. You must meet the ownership and use tests to qualify. Live in the property as your primary residence for at least two of the five years before the sale. The IRS enforces these timelines with zero flexibility. If you're short by even a few days, you could lose the entire exclusion.

Why does 2026 matter? We are currently navigating significant shifts in federal tax brackets. For 2026, the long-term capital gains rates for married couples filing jointly are structured as follows:

- 0% Rate: For taxable income up to $98,900.

- 15% Rate: For taxable income between $98,901 and $613,700.

- 20% Rate: For taxable income exceeding $613,700.

Watch out for the Net Investment Income Tax (NIIT). This 3.8% surtax applies if your modified adjusted gross income tops $250,000 for joint filers. Understanding these tax implications of selling a home in Costa Mesa is non-negotiable for a successful closing.

The California Difference: No Special Rate for Gains

Do not expect a break from Sacramento. California does not offer a lower rate for long-term gains. Every dollar of profit is taxed as ordinary income. Your state liability ranges from 1% to 13.3% based on your total income. Are you selling a high-value asset? If your taxable income exceeds $1 million, you trigger the Mental Health Services Act tax. This adds a 1% surcharge to your total bill. It makes California one of the most aggressive tax environments in the nation. You must factor this into your net proceeds calculation early.

Exceptions to the 2-Year Residency Rule

Did life throw you a curveball? You might qualify for a partial exclusion even if you haven't hit the two-year mark. The IRS allows pro-rated breaks for health issues, job changes that require a move of more than 50 miles, or other unforeseen circumstances. Document everything. You'll need medical records or employment letters to prove a hardship. Are you in the military? Service members can suspend the five-year look-back period for up to ten years while on qualified official extended duty. This ensures your service doesn't drain your home equity.

Calculating Your Costa Mesa Tax Basis: Why Every Upgrade Counts

What is your true net profit? It's not just the sales price minus what you paid years ago. To protect your equity, you must understand your "Adjusted Basis." This figure represents your original purchase price plus the cost of all capital improvements. Think of it as your tax-free foundation. Every dollar you successfully add to your basis is a dollar that escapes taxation when you close escrow. Are you keeping your receipts? If not, you're leaving money on the table.

Costa Mesa residents often overlook the distinction between a repair and an improvement. A repair simply maintains the home's current condition; think of fixing a broken window or patching a leaky roof. These costs are generally not basis-adding. An improvement, however, adds value, prolongs the property's life, or adapts it to a new use. This distinction is a critical factor in the tax implications of selling a home in Costa Mesa. The IRS is strict about this; you need a clear paper trail to justify these adjustments during an audit.

The primary residence exclusion offers a significant buffer, but with Orange County property values soaring in 2026, many sellers find their gains exceeding the $250,000 or $500,000 limits. This is where your meticulous record-keeping pays off. By maximizing your basis, you shrink the taxable "gap" and keep more of your hard-earned wealth. Don't let poor documentation result in an avoidable tax bill.

Common Basis-Increasing Upgrades in Orange County

Are you building an ADU? Constructing a "granny flat" is one of the most effective ways to increase your basis in the current market. In 2026, smart home integrations and high-efficiency solar panel installations also qualify as capital improvements. Even your outdoor living space matters. Landscaping projects, from installing a new pool to designing drought-tolerant coastal gardens, are considered hardscaping that raises your tax foundation. These aren't just aesthetic choices; they are strategic financial maneuvers.

The Cost of Selling: Deductible Transaction Expenses

You don't pay taxes on the gross sales price. You pay on the "amount realized." This means you subtract your selling costs before the tax man takes a cut. Broker commissions, title insurance, escrow charges, and legal fees all act as direct basis adjustments. What about staging and marketing? In 2026, these costs are still recognized as legitimate selling expenses that lower your taxable gain. If you need a professional investment property analysis to determine how these expenses will impact your final check, let's start the conversation.

Costa Mesa Local Taxes: Transfer Fees and Property Reassessments

Do you know who pays the transfer tax in your transaction? In Orange County, the Documentary Transfer Tax is set at $1.10 per $1,000 of the property's value. If you close a deal at $2,250,000, you're looking at a $2,475 charge on your closing statement. While it's standard practice for the seller to cover this in Costa Mesa, everything is negotiable. A seasoned negotiator can often leverage market conditions to shift this cost to the buyer. Don't let these "small" fees eat into your equity without a fight.

Are you aware of the hidden assessments on your title? Mello-Roos and other special assessment districts can create unexpected hurdles. These districts fund local infrastructure like roads and schools, and any outstanding balances must be addressed at closing. Escrow will also handle your property tax prorations. This ensures you only pay for the exact number of days you occupied the home during the current tax cycle. It sounds simple, but errors in these calculations are common. You need a proactive partner to audit these figures before you sign the final papers.

Proposition 13 and the Reassessment Trigger

Selling your home triggers an immediate property tax reassessment for the buyer. Under Proposition 13, your taxes were likely capped at a much lower base than the current market value. The buyer will receive a supplemental tax bill based on the 2026 sales price. Why does this matter to you? It impacts the buyer's monthly carry and your overall leverage. If you're a senior or disabled homeowner, you should explore Prop 19 tax basis transfers. This allows you to carry your current low tax base to a new property, making downsizing a much more attractive financial move.

Withholding Requirements: The FTB Form 593

The biggest shock for many sellers is California’s mandatory 3.33% withholding rule. The Franchise Tax Board (FTB) requires escrow to withhold 3.33% of the total sales price, not just your profit. On a $1.5 million sale, the state could grab nearly $50,000 right at the finish line. Do you qualify for an exemption? Most primary residence sellers do, but you must complete FTB Form 593 accurately to avoid this automatic hit. These tax implications of selling a home in Costa Mesa require precise documentation. Your escrow officer manages the compliance, but the responsibility for the data rests on your shoulders. I make sure you're prepared long before the final 30 days.

Strategic Exemptions for Seniors and Investors: Prop 19 and 1031 Exchanges

Are you ready to move without the tax penalty? Proposition 19 has completely redefined the tax implications of selling a home in Costa Mesa for seniors and the disabled. Before this law, moving often meant a massive jump in property taxes. Now, you can take your low tax base with you. This is a massive win for anyone looking to downsize while keeping their monthly expenses predictable. If you're selling a Residential Care Facility for the Elderly (RCFE), the stakes are even higher. These transactions involve both business assets and real estate, requiring a specialized approach to separate and protect your gains. I’ve spent decades helping facility owners navigate these specific hurdles to ensure their exit is as profitable as possible.

Prop 19 isn't just for primary residences; it's a strategic tool for wealth preservation. For the first time, eligible homeowners can transfer their tax base to a home of any value anywhere in California up to three times. This flexibility allows you to upgrade or downsize without the fear of a tax reassessment ruining your retirement budget. However, the rules for intergenerational transfers have tightened. If you're passing a property to your children, they must use it as their primary residence to keep your low tax base. You need an insider who understands these nuances to avoid a costly reassessment that could drain your family's equity.

Senior Downsizing: Maximizing Your Costa Mesa Sale

Planning your next move requires precision. To maximize your benefit, you need to understand the "Equal or Lesser Value" rule. If your new home costs more than your old one, the difference is added to your transferred tax base. You have a strict two-year window from the date of your sale to complete the purchase of your replacement residence. Don't leave this to chance. Working with a Senior Real Estate Specialist ensures you hit every deadline and satisfy every legal requirement. We specialize in making these complex transitions feel manageable and secure.

The 1031 Exchange: A Tool for Costa Mesa Landlords

For the savvy investor, the 1031 exchange remains the ultimate wealth-building tool. Why pay capital gains now when you can reinvest that money into a larger, more profitable asset? In the 2026 market, identifying "Like-Kind" properties requires an insider's view of non-public inventory. You have exactly 45 days to identify your next property and 180 days to close. These clocks start ticking the moment you close your Costa Mesa sale. You need a 1031 Exchange Broker in Costa Mesa who knows how to move fast and secure the right replacement asset. Ready to secure your legacy? Let’s perform a comprehensive Investment Property Analysis to determine your best path forward.

Navigating the Escrow Process: Closing with Confidence

Are you prepared for the final sprint? The last 30 days of your transaction are where the most critical financial details solidify. You need your documentation ready for the title company long before the moving trucks arrive. Are you tracking the tax implications of selling a home in Costa Mesa down to the last penny? You must. This is the time to gather every receipt and record we discussed in earlier sections to ensure your adjusted basis is beyond reproach. Don't leave your equity to chance in the final hour.

Review the Preliminary Title Report immediately. This document is a window into your property's legal history. We look specifically for tax liens or forgotten encumbrances that could stall your progress. Even a minor clerical error from a decade ago can trigger a delay. My 29 years of local tenure in the Orange County market acts as your best defense here. I’ve seen every possible title hurdle and know exactly how to clear them. We move fast to ensure your title is "clean" so the buyer’s lender stays on schedule.

Check the math on your Closing Disclosure. This is the three page form that outlines exactly where every dollar goes. Look for the property tax prorations and the $1.10 per $1,000 transfer tax we calculated. Are the credits for your capital improvements accurately reflected? Small errors in these line items can lead to significant losses. I audit these figures with you to ensure the "net proceeds" line matches our initial projections. You deserve to sign those final papers with absolute certainty.

Post-Sale Tax Reporting: What Happens Next?

Handing over the keys isn't the final step. You must report the sale on your 2026 federal and state tax returns. Build a "Basis File" today. Keep your closing statement, proof of improvements, and 1099-S forms for at least seven years. This paper trail is your insurance policy against future audits. I coordinate directly with your CPA to ensure they have the specific data needed for a seamless filing. This proactive approach prevents the stress of a last minute scramble during tax season.

The Gregg Perrah Advantage in Costa Mesa

Why settle for a standard transaction when you can leverage an insider's network? I use "off-market" secrets and non-public inventory data to optimize your sale timing for the best possible tax year. Whether you are selling a family residence or need an expert Investment Property Analysis for a care facility, I focus on your maximum ROI. My strategy is built on decades of high-level negotiation and a commitment to immediate response. Stop wondering what your property is worth in this shifting market. Value your Costa Mesa home today!

Secure Your Equity for the Next Chapter

Are you ready to walk away from the closing table with your wealth intact? Mastering the tax implications of selling a home in Costa Mesa is the difference between a successful exit and a massive financial loss. You've learned how to maximize your adjusted basis through careful documentation and how Proposition 19 can protect your property tax base. These aren't just suggestions. They are essential maneuvers in the 2026 market. Why leave your net proceeds to chance when expert guidance is a click away?

With 29+ years of Southern California real estate expertise, I specialize in the high-stakes world of 1031 exchanges, RCFE sales, and senior downsizing. As a Certified Senior Real Estate Specialist (SRES), I provide the seasoned authority you need to navigate complex state and federal laws. My mission is to act as your centralized resource center, making these intricate processes feel manageable and profitable. Let’s ensure your next move is your best move.

Get a Professional Valuation and Tax Impact Analysis for Your Costa Mesa Home

The 2026 market moves fast. Take control of your financial future today and sell with the absolute confidence of an insider.

Frequently Asked Questions

Do I have to pay taxes on the profit from selling my home in Costa Mesa?

You only pay taxes on profits that exceed the federal exclusion limits. Single filers can exclude up to $250,000 and married couples filing jointly can exclude $500,000 if the home was their primary residence for at least two of the last five years. Any gain above these amounts is subject to federal and state taxation. Understanding the tax implications of selling a home in Costa Mesa starts with identifying your specific filing status and residency timeline.

What is the California withholding tax on real estate sales in 2026?

California requires a mandatory withholding of 3.33% of the total sales price at the time of closing. This is not a tax on your profit; it's a prepayment of the estimated state tax due to the Franchise Tax Board. Escrow typically handles this process using FTB Form 593. You may qualify for a full or partial waiver if the property was your primary residence or if you're selling the asset at a loss.

Can I avoid capital gains tax if I use the money to buy a new house?

You cannot avoid capital gains tax on a primary residence just by purchasing a new home. The old "rollover" rules were replaced years ago by the Section 121 exclusion. However, if you're selling an investment property, you can use a 1031 exchange to defer taxes by reinvesting in a like-kind property. This strategy is strictly for business or investment assets; it doesn't apply to your personal residence.

How does Proposition 19 help seniors selling their home in Orange County?

Proposition 19 allows seniors aged 55 and older to transfer their current low property tax base to a new home anywhere in California. This is a game-changer for those looking to downsize without facing a massive property tax hike. You can use this benefit up to three times in your lifetime. It ensures your monthly expenses remain predictable even if you move into a property with a higher market value.

Are home improvements tax-deductible when I sell my Costa Mesa house?

Capital improvements aren't directly deductible from your income, but they do increase your home's "adjusted basis." This higher basis reduces the total taxable gain when you close. You must distinguish between basic repairs and permanent improvements like a new ADU or a kitchen remodel. Keeping meticulous records of these upgrades is vital for minimizing the tax implications of selling a home in Costa Mesa.

What is the difference between federal and California capital gains rates?

The federal government offers preferential rates for long-term capital gains, ranging from 0% to 20% based on your taxable income. California does not offer these special rates. The state taxes all capital gains as ordinary income at progressive rates between 1% and 13.3%. This creates a significant tax burden for high-equity sellers in Orange County, making strategic planning essential before your property hits the market.

How much is the documentary transfer tax in Costa Mesa?

The documentary transfer tax in Costa Mesa is $1.10 per $1,000 of the property's sales price. For a $1,500,000 sale, the tax would be exactly $1,650. While the seller traditionally pays this fee in Orange County, it remains a negotiable item during the escrow process. It's a small but important line item to factor into your final net proceeds estimate before you sign the contract.

What documents do I need to prove my tax basis at the time of sale?

You need your original purchase closing statement and receipts for every capital improvement made during your ownership. These documents establish your starting basis and your final adjusted basis. You should also keep records of all selling expenses, including broker commissions and legal fees. Maintaining a "Basis File" for seven years after the sale protects you in the event of a state or federal audit.