Is the IRS about to become your biggest beneficiary? If you think the standard $500,000 exclusion is enough to protect your equity in a $3.6 million coastal estate, you are in for a shock. You have watched your property value soar. Now, a massive tax bill is waiting to take its cut. Learning how to avoid capital gains tax when selling a house in Newport Beach is the only way to keep your wealth where it belongs. Do not let confusion over California’s 13.3% top tax rate or complex federal rules stall your next move.

I know the pressure of managing high-stakes coastal assets. It feels like the tax landscape shifts every season. This guide promises to hand you the 2026 strategies needed to legally minimize your exposure and shield your hard-earned equity. We will cover everything from maximizing your cost basis to navigating the strict 45-day 1031 exchange window and leveraging Proposition 19. Think of this as your central resource for fiscal clarity. Stop guessing. Start protecting your assets with veteran expertise. It is time to secure your financial future.

Key Takeaways

- Unlock the full potential of the Section 121 exclusion to shield up to $500,000 of your home equity from federal and state tax collectors.

- Master the art of basis maximization by turning your high-end Newport Beach renovations into a powerful tax shield against the IRS.

- Discover the exact steps on how to avoid capital gains tax when selling a house in Newport Beach by utilizing 1031 exchanges for your investment assets.

- Protect family wealth using specialized strategies for seniors and heirs, including the nursing home use exception and the step-up in basis.

- Leverage over 26 years of local market expertise to execute high-stakes negotiations that prioritize your net proceeds and long-term fiscal security.

The Section 121 Exclusion: Is Your Newport Beach Equity Protected?

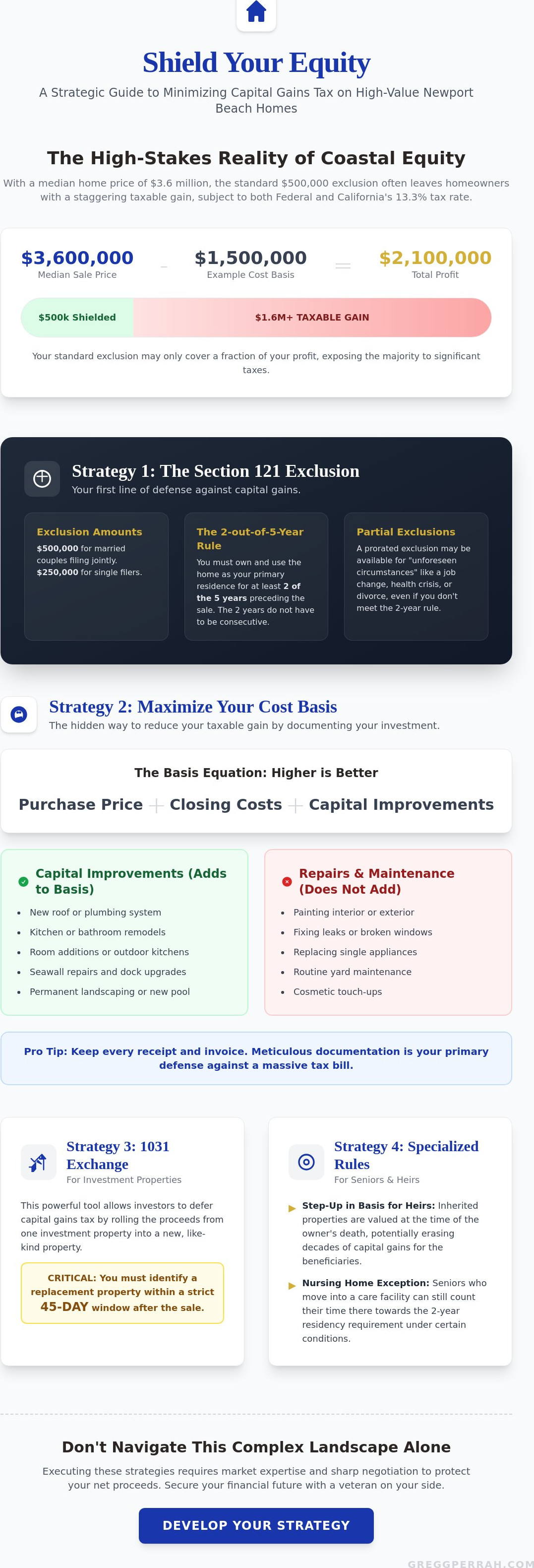

Are you sitting on millions in equity? If you own a home in Crystal Cove or Lido Isle, you likely are. The Section 121 exclusion is the most common tool used by homeowners, but it's often misunderstood. For 2026, the rules remain firm. Single filers can exclude $250,000, while married couples filing jointly can shield $500,000 of profit from federal and state taxes. But here is the reality: with Newport Beach median home prices hitting $3.6 million, that $500,000 threshold is barely a start. Understanding Capital gains tax in the United States is vital because the IRS doesn't care about the coastal lifestyle; they care about the math. To qualify, you must meet the Ownership and Use test. This means you lived in the property as your primary residence for at least two of the five years before the sale. It is a simple rule with massive implications for your bottom line.

The 2-Out-Of-5 Year Rule in Coastal Markets

Timing is everything when you want to know how to avoid capital gains tax when selling a house in Newport Beach. You don't need to live there for the final two years consecutively. You just need 730 days of residency within the five-year window. Did you move from the Peninsula to a rental property? You can still claim the full exclusion if you sell within three years of moving out. However, if you converted your home to a rental, be careful. You might face depreciation recapture taxes. I've seen homeowners lose thousands because they waited just one month too long to list. Don't be that person. Get the timing right and protect your cash.

Partial Exclusions: Can You Still Save?

Life happens. Sometimes you can't hit that two-year mark. Do you lose everything? Not necessarily. The IRS allows for "unforeseen circumstances." If a health crisis, job change, or divorce forces a move from Orange County, you may qualify for a prorated exclusion. For example, if you lived in your Corona Del Mar home for only one year due to a job relocation, you might still exclude half of the maximum amount. Even if you're selling "As-Is" to a developer, these primary residence benefits still apply. You need a veteran who understands these nuances to ensure you aren't leaving money on the table. Knowing how to avoid capital gains tax when selling a house in Newport Beach requires looking at every possible deduction. Every dollar of equity belongs in your pocket, not the government's.

Maximizing Your Cost Basis: The "Hidden" Way to Reduce Tax

Are you overlooking your most powerful tax shield? In a market where the median home price sits at $3.6 million, the standard federal exclusion is just the beginning. You need to master your Adjusted Cost Basis. This figure represents your total investment in the property. It starts with the original purchase price. Then you add closing costs, legal fees, and every major capital improvement you've completed. The higher your basis, the lower your taxable gain. This is the most effective strategy for how to avoid capital gains tax when selling a house in Newport Beach. Don't leave your equity to chance. Demand fiscal clarity before you list.

Consult IRS Publication 523 for the specific rules on what qualifies as a capital improvement. In the luxury coastal market, your renovations are more than just aesthetic choices. They are calculated financial maneuvers. Did you add a custom wine cellar? Did you install a professional-grade outdoor kitchen? These are capital improvements because they add permanent value and prolong the property's life. Keep every receipt and track every invoice. This documentation is your primary defense against a massive tax bill. Every dollar added to your basis is a dollar shielded from the IRS and the California Franchise Tax Board.

Deductible Improvements vs. Maintenance

Distinguishing between a simple repair and a capital improvement is critical. Fixing a leaky pipe is maintenance. It keeps the home in its current state. The IRS won't let you add that cost to your basis. However, replacing the entire plumbing system or installing a new roof is a capital improvement. In Newport Harbor, seawall repairs and dock upgrades are massive expenses that significantly boost your basis. Even smart home technology installations in 2026 add to your financial shield. If it adds permanent value or adapts the home to a new use, it's a tax win. Stop guessing and start documenting your investments.

Selling As-Is: How It Affects Your Taxable Gain

Is a pre-sale renovation always the right move? Not necessarily. This is the Renovation Trap. You might spend $200,000 on a kitchen that only adds $150,000 in market value. In these high-stakes scenarios, selling as-is can be the superior strategy. You can offer repair credits to the buyer. This effectively lowers the final sales price. A lower sales price results in a smaller capital gain. It's a calculated move often seen when reviewing Newport Beach real estate listings for "fixer" potential. You need a veteran negotiator who understands these fiscal nuances. If you need a professional analysis of your property's value, reach out today. Every dollar of your equity belongs in your pocket.

The 1031 Exchange: Deferring Taxes on Investment Properties

What if you could sell your Balboa Peninsula rental and pay zero taxes? It is not a dream; it is a strategic maneuver. You just need to follow the 1031 Exchange Rules. This strategy isn't reserved for commercial skyscrapers. It's for your Newport Beach portfolio. By swapping your property for a "like-kind" asset, you defer the capital gains tax indefinitely. You could trade a luxury condo for a cash-flowing RCFE facility or a multi-unit complex. This is the ultimate move for savvy investors who want to keep their wealth working. Why hand over 20% or more to the government when you can reinvest it?

The clock is your primary enemy in this process. You have exactly 45 days from the date of your sale to identify a replacement property in writing. After that, you have a total of 180 days to close. If you miss these deadlines by even one hour, the IRS will demand their cut. You need a 1031 exchange broker in Costa Mesa who understands the urgency of the OC market. We specialize in finding non-public inventory that fits your specific tax-deferral needs. Speed and precision are the only ways to win this game.

The "Primary to Rental" Conversion Strategy

Have you lived in your Newport home for decades? If your gain is $2 million, the standard $500,000 exclusion leaves $1.5 million exposed to heavy taxation. Here is a veteran secret. Move out and rent the home for at least two years. This qualifies the property as an investment asset. You can then use the Section 121 exclusion to take $500,000 tax-free and use a 1031 exchange to defer the remaining $1.5 million. This hybrid approach is how to avoid capital gains tax when selling a house in Newport Beach while maximizing your net proceeds. It's about playing the long game with your equity.

DSTs and Passive Reinvestment Options

Are you tired of managing tenants and toilets? Delaware Statutory Trusts (DSTs) offer a way to "retire" from active landlording while still satisfying 1031 requirements. You reinvest your proceeds into a fractional interest of high-quality, professionally managed real estate. It's a passive solution for those who want the tax benefits without the stress. Start with a comprehensive investment property analysis to see if a DST matches your financial roadmap for 2026. Don't let your equity sit idle. Make it work for you.

Specialized Strategies for Seniors and Heirs

Are you planning a late-life move or managing a family estate? Protecting a legacy in Newport Beach requires more than just a standard listing. For seniors transitioning into care, the IRS offers a critical loophole often overlooked by general agents. While most homeowners must meet the two-year residency rule, the Nursing Home Exception allows you to qualify for the full Section 121 exclusion with just one year of use. If you've lived in your home for at least 12 months and then moved into a licensed facility, you can still shield up to $500,000 of profit. This is a game-changer for families facing high medical costs. It's a vital part of how to avoid capital gains tax when selling a house in Newport Beach without rushing a sale during a health crisis.

What happens to the remaining equity? If you're an heir, the "Step-up in Basis" is your most powerful ally. When you inherit a property, its cost basis is reset to the fair market value at the time of the owner's death. If a parent bought a Balboa Island cottage for $100,000 in 1970 and it's now worth $4 million, your new basis is $4 million. You could sell it immediately and owe zero capital gains tax. However, under California's Proposition 19, you must move into the property as your primary residence within one year to keep the low property tax assessment. Navigating these overlapping federal and state rules is complex. You need a veteran who handles these high-stakes coastal assets every day.

The Senior Real Estate Specialist (SRES) Advantage

Why settle for a generalist when your family's wealth is on the line? A Senior Real Estate Specialist understands the emotional and financial weight of downsizing. We don't just put a sign in the yard. We coordinate with your estate attorneys and tax professionals to ensure every move is optimized. Whether you're looking at an RCFE for sale or a smaller coastal condo, our goal is to reduce your stress. We provide the fiscal clarity you deserve during a major life transition. If you're ready to explore your options, contact us for a confidential property assessment.

Prop 19 and the California Tax Portability

Proposition 19 is a massive benefit for homeowners over 55. It allows you to transfer your low property tax base from your current Newport Beach home to a new residence anywhere in California. You can do this up to three times. This complements your strategy for how to avoid capital gains tax when selling a house in Newport Beach by ensuring your monthly carrying costs remain low in your new home. Whether you're moving to a smaller property in Orange County or a vineyard in Temecula, you keep your tax advantage. This is about more than just one sale. It's about your long-term financial freedom. Don't leave your tax base behind when you move. Take it with you.

The Gregg Perrah Strategy: Execution and Negotiation

Why trust a generalist with your most significant financial asset? Mastering how to avoid capital gains tax when selling a house in Newport Beach isn't just about reading a guide. It is about elite execution and high-stakes negotiation. With over 26 years of professional longevity, Gregg Perrah | FirstTeam Real Estate has navigated every market cycle Orange County has faced. We don't just list properties. We provide a "tireless, always-on" commitment to your financial success. This means providing a comprehensive financial assessment of your coastal asset before a single photo is taken. We analyze your equity, your potential tax exposure, and your reinvestment goals to build a custom roadmap. Success here requires an insider who can find the non-public inventory and off-market investment opportunities that others miss.

You deserve a negotiator who understands the nuances of the California Franchise Tax Board and the IRS. The approach of Gregg Perrah | FirstTeam Real Estate is rooted in seasoned authority and proactive energy. We don't wait for the market to come to us. We create the market. This is the hallmark of a sophisticated resource center. We provide the keys to a network built over three decades. Stop wondering what your home is worth. Start understanding how much of that value you can actually keep. Protecting your wealth is our primary engagement strategy. It is time to move from inquiry to action.

Beyond the Listing: A Comprehensive Resource Center

Luxury real estate isn't just about high-end photography and global branding. In 2026, the best luxury real estate agents must function as sophisticated knowledge bases. They must understand the intersection of real estate law and tax strategy. By leveraging the power of the Gregg Perrah | FirstTeam Real Estate network, we ensure your property receives maximum exposure while maintaining fiscal clarity. We handle the complexity so you don't have to. Are you ready to see the real numbers? Get your Newport Beach asset valuation today and see the difference that local tenure makes.

Ready to Sell? Start Your Strategic Consultation

The best time to plan your exit was yesterday. The second best time is right now. We start by auditing your cost basis to ensure you aren't overpaying the IRS. This is the fundamental step in how to avoid capital gains tax when selling a house in Newport Beach. We identify the specific exit strategy for your neighborhood, whether you are in the Port Streets or Big Canyon. Every asset is unique. Every tax situation is personal. Don't settle for a cookie-cutter sales plan. Contact Gregg Perrah | FirstTeam Real Estate for an immediate response on your property valuation. Let's secure your equity and your future today.

Take Command of Your Fiscal Future

Your Newport Beach equity is too valuable to leave to chance. We've covered why the standard Section 121 exclusion is just the beginning of a real tax strategy. You now understand that maximizing your cost basis and executing precise 1031 exchanges are the true keys to wealth preservation. Whether you're a senior utilizing Prop 19 or an heir managing a legacy estate, the objective remains the same. You must master how to avoid capital gains tax when selling a house in Newport Beach to ensure your hard-earned wealth stays with your family, not the government.

I provide 26 years of local Newport Beach tenure to guide you through these complex market cycles. As a Senior Real Estate Specialist (SRES) and an expert in 1031 exchange facilitation, I offer the seasoned authority required for high-stakes coastal assets. It's time to stop guessing and start executing. Get Your Newport Beach Asset Valuation & Tax Strategy Session today. Let's secure your proceeds and your future with the proactive energy your portfolio deserves. You've worked hard for your equity; don't let it slip away.

Frequently Asked Questions

Can I avoid capital gains tax if I sell my Newport Beach home and buy another one?

Simply buying a new home does not defer your tax liability. The old "rollover" rule was replaced decades ago by the Section 121 exclusion. You can shield $250,000 as an individual or $500,000 as a married couple, but the purchase of a replacement residence doesn't offset the remaining profit. This is why mastering how to avoid capital gains tax when selling a house in Newport Beach through basis maximization is your only real defense.

How does the 2-out-of-5-year rule work for married couples in California?

To claim the full $500,000 exclusion, both spouses must meet the "use" test by living in the home for at least two of the five years before the sale. However, only one spouse needs to meet the "ownership" test. California law conforms to these federal requirements. If one spouse lived elsewhere during that window, your exclusion could be slashed to $250,000. Don't leave your equity to chance; verify your residency dates now.

What capital improvements are tax-deductible when selling a house?

Capital improvements add permanent value or adapt the property to new uses. Think of major kitchen remodels, infinity pools, new seawalls, or professional landscaping. Routine repairs like fixing a leaky faucet or painting a room for maintenance do not count. You must add the cost of these major projects to your initial purchase price to increase your cost basis. Keep every receipt. These documents are your primary shield against the IRS.

Can I use a 1031 exchange for my primary residence in Newport Beach?

You cannot use a 1031 exchange for a property you currently use as your primary residence. These exchanges are strictly for investment or business assets. However, you can convert your home into a rental for at least two years to unlock this eligibility. This allows you to use the Section 121 exclusion and the 1031 exchange together. It is a sophisticated maneuver that requires veteran guidance to execute correctly in the 2026 market.

What is the capital gains tax rate for high-income earners in California for 2026?

High-income earners face a heavy combined tax burden in 2026. California taxes capital gains as ordinary income, which can reach a top rate of 13.3%. On the federal side, you likely face a 20% long-term capital gains rate plus the 3.8% Net Investment Income Tax. When your Newport Beach property appreciates by millions, your total effective tax rate can exceed 37%. You need a proactive strategy to protect your net proceeds from this hit.

What happens if my capital gain is higher than the $500,000 exclusion?

Any profit exceeding the $500,000 exclusion is fully taxable at the applicable federal and state rates. In Newport Beach, where the median price is $3.6 million, many sellers find themselves in this "excess gain" category. This is where your adjusted cost basis becomes vital. By meticulously adding every renovation and closing cost to your basis, you reduce the taxable portion of your gain. Every dollar of documentation saves you roughly 37 cents in taxes.

Is there a tax exception for seniors moving into assisted living or RCFEs?

Yes, the "one-year rule" provides a significant exception for seniors. If you lived in your home as a primary residence for at least 12 months and then moved into a licensed care facility, you can still qualify for the full Section 121 exclusion. This is a critical part of how to avoid capital gains tax when selling a house in Newport Beach during a health transition. It ensures you don't lose your tax benefits just because you needed professional care.

Do I have to pay California state tax on my home sale if I move out of state?

You must pay California tax on the sale regardless of where you move. California taxes all income sourced within the state, including the sale of real property located in Newport Beach. Moving to a tax-free state like Nevada or Florida before you close does not exempt you from the California Franchise Tax Board's reach. Plan for this state-level hit as part of your overall exit strategy to avoid an expensive surprise at tax time.