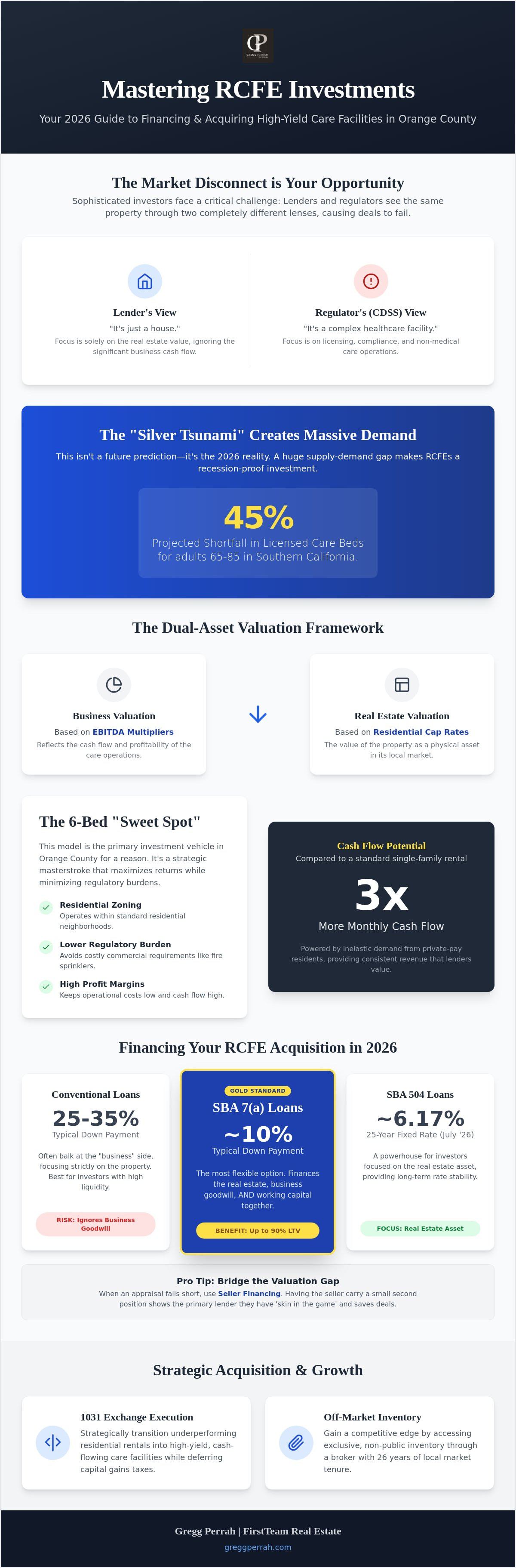

Why are so many sophisticated investors failing to close on 6-bed facilities in Orange County right now? Most lenders look at your application and see a simple house, while the CDSS sees a complex healthcare facility. This disconnect is the primary reason financing an RCFE purchase in California feels like a constant uphill battle. You already know these assets are gold mines for cash flow, but the dual-asset nature of the property makes traditional banks nervous. You need a strategy that respects both the real estate value and the business EBITDA.

I've spent 26 years navigating these high-stakes negotiations. I'm telling you that the 2026 market requires a sharper, more aggressive approach. This guide will show you how to master the complexities of RCFE financing by using a framework that separates business value from real estate assets. We'll explore how to deploy 1031 exchange funds to maximize tax-deferred growth while avoiding the licensing delays that frequently kill escrows. From current SBA 7(a) rate ranges to finding off-market inventory through a veteran network, you're about to get the insider keys to the kingdom.

Key Takeaways

- Identify why the "Silver Tsunami" is driving unprecedented demand for senior housing beds across Southern California in 2026.

- Navigate the specific requirements for financing an RCFE purchase in California by leveraging SBA 7(a) and 504 loan structures.

- Apply the Dual-Asset Valuation framework to accurately separate business EBITDA multipliers from residential real estate cap rates.

- Execute a strategic 1031 exchange to transition underperforming residential rentals into high-yield, cash-flowing care facilities.

- Gain a competitive edge by accessing exclusive, non-public inventory through a broker with 26 years of local market tenure.

Understanding RCFE Investments in the 2026 California Market

What is an RCFE? It stands for Residential Care Facility for the Elderly. These are Residential Care Facilities that provide non-medical, assisted living services. In 2026, the California market has hit a tipping point. The "Silver Tsunami" isn't a prediction anymore; it's a reality. Southern California is projected to face a 45% shortfall in licensed care beds for adults aged 65-85 this year. This massive supply-demand gap makes financing an RCFE purchase in California a high-priority move for serious investors. Are you ready to capitalize on this demographic shift? You should be. The numbers don't lie.

Aging is inevitable. This simple fact makes RCFEs recession-proof real estate investments, especially in high-equity areas like Orange County. Unlike retail or office space, senior housing demand remains inelastic regardless of interest rate cycles. You have two primary ways to enter this market. You can acquire the business operations only, or you can secure the "Property + Business" model. The latter is where the real wealth is built. By owning both the real estate and the cash-flowing care business, you create a dual-asset shield that protects your capital while maximizing monthly returns. Look at the current landscape. With over 7,800 licensed facilities in the state, the competition is fierce, but the rewards for those who secure financing are substantial.

The 6-Bed Facility Standard

Why stop at six? In residential neighborhoods throughout Newport Beach and Costa Mesa, the 6-bed facility is the primary investment vehicle. Staying under the 7-bed regulatory threshold is a strategic masterstroke. It allows you to operate within residential zoning without the heavy commercial fire sprinklers and safety requirements of larger institutions. This keeps your operational costs low and your margins high. The 6-bed RCFE is the sweet spot for individual investors seeking high margins without the headache of institutional-scale management. It's a manageable, high-yield asset that fits perfectly into a quiet cul-de-sac.

Inelastic Demand in Southern California

Compare a standard single-family rental in Costa Mesa to an RCFE. A traditional rental might net you a few thousand dollars a month after expenses. An RCFE with private-pay residents can triple that cash flow. Senior care remains in high demand even when the economy stutters. Families will cut luxury spending, but they won't compromise on care for their parents. This is why private-pay resident models are the engine behind facility valuation in 2026. They provide the fiscal clarity and consistent revenue that lenders demand when you're looking at financing an RCFE purchase in California. Don't settle for low-yield rentals when you can secure a cash-flowing care asset with built-in demand.

Financing an RCFE Purchase in California: SBA vs. Conventional Loans

Capital is the lifeblood of your acquisition. In 2026, the SBA 7(a) loan remains the gold standard for financing an RCFE purchase in California because it allows you to finance the business goodwill alongside the real estate. Conventional lenders often balk at the "business" side of a care home. They prefer the safety of the bricks and mortar. Most conventional commercial loans for care facilities now require a 25% to 35% down payment. If you want to keep your liquid cash for operational reserves, the SBA 7(a) is your best friend. It offers a path to ownership that conventional banks simply can't match for first-time facility buyers.

For investors focusing strictly on the real estate asset, the SBA 504 loan is a powerhouse. As of July 2026, 25-year fixed rates for the 504 program are hovering around 6.17%. This provides long-term stability in a market where the prime rate is currently 6.75%. However, what happens when the bank appraisal doesn't meet the seller's asking price for the business's "goodwill"? This is where seller financing for RCFE purchase becomes essential. By having the seller carry a small second position, you bridge the valuation gap and signal to your primary lender that the current owner has skin in the game. It’s a classic move that saves deals every day in Orange County.

SBA 7(a) Loan Specifics for 2026

The SBA 7(a) is incredibly flexible. It covers the purchase of the business, the property, and even working capital. You can often secure up to 90% Loan-to-Value (LTV) for healthcare-related real estate. This allows you to leverage your capital further than any other product. One critical update for 2026: SBA lenders now strictly require that the borrower has documented management experience or a qualified, licensed administrator on the team at the time of application. Without this, your file will likely be dead on arrival. Don't let a lack of paperwork stall your escrow.

Bridge Loans and Private Capital

Speed costs money. When an off-market opportunity in Costa Mesa hits your desk, you might not have 90 days for SBA processing. Bridge financing allows you to close in as little as 21 days. The interest rates are higher, often 3% to 5% above conventional rates, but they provide the "buy now, refinance later" capability required in a competitive market. This is a common tactic for investors moving from a traditional single-family rental into a high-yield care facility via a 1031 exchange. You secure the asset first, then transition into a permanent SBA position once the license transfer is complete. Ready to see which lenders are actually funding 6-bed homes in Newport Beach right now? Let's look at your investment property analysis together.

The Dual-Asset Valuation: Balancing EBITDA and Real Estate Cap Rates

Stop looking at the gross income. It's a trap. Financing an RCFE purchase in California requires a surgical look at the net operating income. You aren't just buying a deed; you're buying an EBITDA stream. Lenders understand this dual-asset nature better than most novice investors. That's why they demand two separate reports: a business valuation for the operations and a residential appraisal for the dirt. If these two numbers don't align, your deal dies at the underwriting desk. I've seen it happen dozens of times. You need a strategy that justifies the premium price tag of a licensed facility.

How do we determine the business value? We use EBITDA multipliers. In the 2026 market, 6-bed homes typically trade at 3x to 5x adjusted EBITDA plus the value of the real estate. Larger facilities with 15 to 49 beds can command 5x to 8x. But remember, the real estate value is still anchored to local Orange County residential comps. If a house in Newport Beach is worth $2 million as a residence, but the RCFE business generates $300,000 in annual profit, the total acquisition price must reflect that combined reality. Balancing these two distinct valuations is the only way to secure the leverage you need.

Normalizing Financials for EBITDA

How do you find the real money? You look for add-backs. Many owner-operators run personal expenses through the business, from car leases to family cell phone plans. You must strip these away to find the true profit. In 2026, you also have to account for aggressive California labor law enforcement and rising minimum wage impacts on your margins. Blue sky value represents the facility's license and reputation, essentially the premium you pay for a turnkey operation that is already generating cash. Don't leave money on the table because you failed to normalize the books.

Cap Rate Trends in Newport Beach and Costa Mesa

RCFE properties command lower cap rates than standard rentals because the income density is significantly higher. While a traditional condo in Newport Beach might see a 4% cap rate, a stabilized RCFE facility in 2026 often sees cap rates between 7% and 10%. This is why financing an RCFE purchase in California is so attractive to 1031 exchange investors. Specialized upgrades like ADA compliance and industrial fire sprinklers aren't just costs; they are massive value-adds that protect your license and increase the property's utility. Check out the latest Commercial Property for Sale Costa Mesa: 2026 Market Trends & Investment Secrets to see how these specialized assets are outperforming the broader commercial market right now.

Are you confused by the math? Don't be. My investment property analysis service breaks down these multipliers so you know exactly what you're paying for. We analyze the tax returns, the census, and the property condition to ensure the dual-asset value is rock solid before you sign the contract.

Strategic Acquisition: 1031 Exchanges and Off-Market Inventory

Are you tired of low-yield residential rentals? Swapping a standard single-family home for a high-yield care facility is a professional power move. Using a 1031 exchange to facilitate financing an RCFE purchase in California allows you to defer massive capital gains taxes while stepping into a superior cash-flow position. The IRS "Like-Kind" rule is your greatest ally here. Even though an RCFE includes a business component, the underlying residential real estate qualifies for tax-deferred treatment. This means you can roll 100% of your equity from a beach condo or a suburban rental directly into a licensed care home without taking a tax hit on the property value.

Timing is everything in this game. You have exactly 45 days to identify your replacement property and 180 days to close. In a market as tight as Orange County, 45 days is a heartbeat. If you wait until your current rental closes to start looking for a facility, you've already lost. You need a pipeline of inventory ready to go. Because of the specialized nature of these assets, understanding the tax implications of financing an RCFE purchase in California ensures you don't lose 30% of your equity to the government. You need a veteran who can align these windows perfectly.

Maximizing Tax-Deferred Growth

Success requires a Qualified Intermediary (QI) who understands the dual-asset nature of these deals. You must clearly separate the purchase price between the real estate and the business goodwill, as only the real estate portion qualifies for the 1031 exchange. A mistake here can trigger a massive audit. For a deeper dive into the acquisition process, read my RCFE for Sale: The 2026 Strategic Guide to Buying Care Facilities in Southern California. It breaks down how to structure these complex offers to satisfy both the IRS and your lender.

Accessing Non-Public Inventory

Why aren't the best deals on public portals? Confidentiality is the lifeblood of a successful care home. Sellers know that a "For Sale" sign scares away staff and makes resident families nervous. They won't list publicly. They rely on "pocket listings" shared only with a trusted inner circle. My 26-year network in Newport Beach and Costa Mesa uncovers these unlisted healthcare assets before they ever hit the open market. The 'Off-Market Premium' represents the immense value of operational stability maintained by keeping the sale private during the transition. Don't settle for the leftovers on public sites. Contact me to access current off-market RCFE opportunities and secure an asset that actually performs.

Securing Your RCFE Investment with a 26-Year SoCal Veteran

Experience isn't just a number on a resume; it's the safety net for your capital. I've been navigating the complexities of the Southern California market since 1997. That's nearly three decades of surviving market crashes, shifting interest rate cycles, and evolving state regulations. When you choose Gregg Perrah | FirstTeam Real Estate, you aren't just hiring an agent. You're tapping into a centralized resource center that pairs institutional strength with the specialized expertise required for healthcare assets. We know how to look past a polished P&L to find the operational reality of a facility. This deep-dive analysis is what separates a high-yield asset from a financial liability in the competitive Orange County landscape.

My approach is unapologetically proactive and sales-forward. I've spent my career building a network of lenders, DSS consultants, and licensed administrators who know how to get deals done. We don't wait for problems to arise during escrow. We anticipate them. This level of seasoned authority is what makes complex healthcare transactions feel manageable for my clients. You aren't just gaining a broker; you're gaining access to a comprehensive knowledge base designed to maximize your ROI in the 2026 market. We ensure every piece of the puzzle, from the real estate appraisal to the business valuation, aligns perfectly for your lender.

The SRES and 1031 Specialist Advantage

Why do standard residential agents fail in the RCFE space? They don't understand the "dual-asset" valuation model we've analyzed. They treat these like standard homes, which is a recipe for disaster at the underwriting desk. As a Senior Real Estate Specialist (SRES) and an expert in 1031 tax-deferred exchanges, I provide the technical knowledge needed to structure these deals correctly from day one. We connect our clients to a verified network of lenders who actually understand 6-bed facilities. This insider access is vital when you're financing an RCFE purchase in California, as it ensures your loan application reflects the true value of both the real estate and the business goodwill. Don't risk your 45-day identification window on an amateur who is learning on your dime.

Immediate Response Strategy

Speed is the ultimate currency in Newport Beach and Costa Mesa. High-performing facilities rarely hit the public market; they're snatched up in "pocket listings" before the ink is dry on the contract. My "always-on" commitment means you have a tireless negotiator in your corner at all hours. You get direct access to my acquisition strategy and a network that has been growing since the late 90s. We move with the urgency that high-stakes transactions demand. If you're ready to move from investor to owner, don't settle for second-best. Ready to act? Contact Gregg Perrah | FirstTeam Real Estate today to secure your investment and build your legacy in the California senior care market.

Secure Your Future in the 2026 Senior Care Market

The 2026 senior housing market doesn't wait for the hesitant. Success requires a surgical approach to valuation and a deep understanding of the Dual-Asset framework. You now have the blueprint for financing an RCFE purchase in California by balancing EBITDA multipliers with residential cap rates. Whether you're deploying 1031 exchange funds or securing an SBA 7(a) loan, the goal is clear. You must capture the massive demand created by the Silver Tsunami before your competition does.

I've spent my career navigating these complex market cycles. Since 1997, I've been a boots-on-the-ground advocate for investors in Newport Beach and Costa Mesa. As a Senior Real Estate Specialist (SRES) and expert in 1031 tax-deferred exchanges, I offer more than just a listing service. I provide a centralized resource center to help you identify, value, and acquire high-performing care facilities that never see the public light of day. Are you ready to move?

Stop browsing public scraps. Get the non-public RCFE inventory from Gregg Perrah today.

Your next high-yield asset is waiting for you. Let's go get it.

Frequently Asked Questions

How long does it take to get an RCFE license transfer in California in 2026?

A license transfer generally takes 60 to 120 days in 2026. The CDSS is currently in a period of aggressive statewide enforcement, so any errors in your application will trigger significant delays. Most investors use a management agreement to begin operations while the official license transfer is pending. This allows the business to continue generating cash flow during the transition.

Can I use a 1031 exchange to finance both the RCFE business and the real estate?

You can only use 1031 exchange funds for the real estate portion of the deal. The business goodwill and equipment are not considered "like-kind" property under IRS rules. You must bifurcate the purchase price and use other capital or financing for the business acquisition. This ensures you don't trigger a massive tax penalty on your exchange.

What is the minimum down payment for an SBA 7(a) loan on an RCFE?

The minimum down payment is 10% for an SBA 7(a) loan. This 90% LTV is the highest leverage available for financing an RCFE purchase in California. It is specifically designed to help investors acquire both the property and the cash-flowing business operations. Keeping more cash in your pocket is essential for maintaining the operational reserves lenders require in 2026.

Do I need a medical background to qualify for RCFE financing?

No, a medical background isn't mandatory. However, SBA lenders in 2026 strictly require that you have management experience or a qualified administrator on your team. They want to see a clear plan for operational oversight. If you don't have a background in care, hiring a veteran administrator is the fastest way to secure loan approval.

What are the staffing requirements for a 6-bed facility in Orange County?

You must have at least one caregiver on duty 24/7 for a 6-bed facility. Additionally, you need a licensed administrator to oversee operations and resident care plans. Labor laws are being strictly enforced in 2026, so you must budget for competitive wages. Retaining a consistent staff is the best way to maintain the high census numbers that lenders look for.

What is the difference between an RCFE and an Adult Residential Facility (ARF) for financing?

RCFEs serve seniors age 60 and older, while ARFs serve adults with disabilities aged 18 to 59. Lenders often prefer RCFEs because the "Silver Tsunami" provides a more predictable demand curve. This stability makes it easier to secure aggressive terms when financing an RCFE purchase in California. The elderly care model is generally viewed as more recession-proof than the ARF model.

Are fire sprinklers required for all RCFEs in California?

Fire sprinklers are required if you intend to house non-ambulatory residents. Even if your current residents are ambulatory, installing sprinklers is a massive value-add for the real estate. It broadens your potential resident base and makes the facility more attractive to future buyers. Lenders view these specialized safety upgrades as a way to protect their collateral.

How do I value the 'goodwill' of an existing care facility for a lender?

Goodwill is valued using adjusted EBITDA multipliers, which typically range from 3x to 5x for 6-bed homes. You must identify "add-backs" like personal car leases or non-essential owner expenses to show the true profit. Lenders require a formal business valuation report that is separate from the real estate appraisal. This report justifies the "blue sky" premium you are paying for the operation.